It is the end of 2025, and the national real estate market has been slowing for the last several years. A major cause of this is the increase in mortgage rates that are forcing many would-be buyers out of the market and causing many would-be sellers to sit tight with their sub 4.0% interest rates.

So when might the mortgage rates change? In short, no one can be sure.

According to Freddie Mac, the average 30-year fixed rate is currently about 6.18%. A lot of the news cycle follows the Federal Reserve Board and their decisions to raise or lower interest rates. This is somewhat of a red herring for mortgage rates.

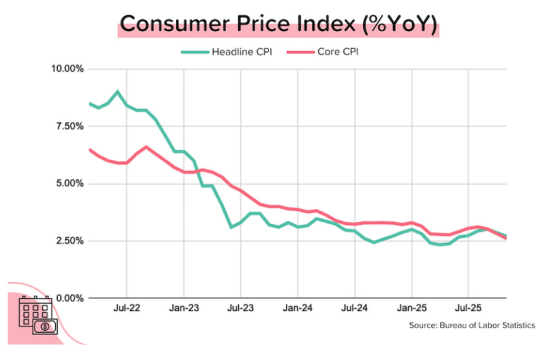

The Fed began raising interest rates several years ago when inflation had grown out of control. The result has been very effective, as seen in the CPI graph. The core CPI has dropped from over 7.0% to under 2.75%.

The Fed is also watching employment numbers. The broader unemployment numbers rose from 8.0% in September to 8.7% in November. No statistics were available in the month of October due to the government shut down.

So, with inflation down and unemployment up, it seems the economy has cooled enough that the Fed can reduce interest rates, and many analysts expect a decision to due so by March However, the Fed does not directly affect mortgage rates. Mortgage rates often drop when the Fed announced their plans to drop rates, but when the board actually follows through with a cut, mortgage rates often jump up for weeks.

The mortgage rates are actually more closely associated with the bond market. Investors looking for long-term lower-risk gains often look at bond and mortgage-backed securities. Being backed by the federal government, bonds appear more secure. To attract those investors, mortgages must provide higher interest to those investors and, in turn, charge homebuyers more. When bond rates, and therefore mortgage rates, will decline is much more difficult to predict.

So, what is a potential buyer to do? Don't obsess over the mortgage rate. As long as you can afford the payment, don't try to time the market. Work with your lender to get the best rate you can and make your home purchase. In the future, the mortgage rates may drop, and you can refinance to the lower rate. Or mortgage rates may rise, and you will be glad you got in at 6.18%.